This is the second article in a 2-post series — the first one covering Facebook can be found here.

When I was originally planning this series, I wanted to cover — and contrast — two companies that had recently started to experience peculiarly similar issues, but in my mind were nonetheless facing completely different challenges and outcomes going forward, despite some obvious similarities in their current states, thus creating an interesting case for comparison. Those companies were Facebook and Apple.

I’ already wrote a lengthy post about Facebook a few weeks back, and given how some of the recent developments made parts of my Apple write-up unnecessary (as the things I intended to cover have already played out), so I decided to make this post a bit less focused on the stock valuation aspects, and instead to spend more time brainstorming on the challenges and opportunities I believe Apple is going to face going forward.

Apple: a trillion dollar company of a single product

Today, Apple’s story is almost legendary — the company almost went bankrupt in 1997, and was worth less than $5 billion in 2000, but then went on to rise to the valuation of $150 billion by 2007, and then again to the top spot of the most valuable publicly traded company in the world in 2012, finally becoming the first publicly traded company to surpass the coveted $1 trillion number.

While one might argue that Apple started on the path of becoming the company it is today with the launch of iMac in 1998, it seems a bit more fair to say that it was actually the iPod, announced in 2001, that clearly signaled the beginning of the new era for Apple, followed by iTunes Store (called “iTunes Music Store” back then) that launched in 2003, and finally, the original iPhone, introduced in 2007. From there, Apple has gone to become the most valuable company in the world and has built what it is perhaps the largest (and for sure the most profitable) consumer tech business of all times, culminating with its market capitalization surpassing $1.1 trillion by the end of September 2018.

And yet, after the announcement of Q3 results (well, Q4 in Apple’s case, because of how its financial year aligns to the calendar one) on November 1, its share price fell more than 7%, constituting the worst decline since 2014, amidst a widespread investor backlash around Apple’s decision to stop reporting the number of devices sold starting next quarter.

So far, the stock price hasn’t demonstrated any signs of recovery; instead, the ensuing news about weaker than anticipated demand for new iPhones dragged the stock price even lower, and as of the close yesterday (December 17), Apple's stock was worth less than $164, down almost 30% from its 52-week high of $233.47 (to be fair, part of the decline could be attributed to the horrible performance of the broader markets in the last few months, but still, Apple’s stock performance was much worse compared to the overall market in that time frame). This decline led Apple to lose the top spot as the most valuable company, passing this title, as luck would have it, to Microsoft, which weathered the volatility of the last few months somewhat better than other big tech companies.

It’s not particularly hard to figure out the nature of the issue Apple’s facing — in fact, it can be summarized in a single chart:

Source: Statista.com

As you can see here, it’s been now 4 years since the number of iPhones sold has delivered any growth, which, coupled with the fact that iPhone sales account for about 60% of Apple’s overall revenue, poses an obvious problem for the company.

Over the last year or so, the introduction of iPhone X, and then of iPhones XS and XS Max, has helped the company to temporarily address those concerns by substantially increasing the average selling price of an iPhone ($793 in Q4 2018, vs. only $618 a year ago). Still, the broader issue remains largely unsolved — with iPhone sales stagnant, and iPhone accounting for such a large percentage of the overall revenue, it’s hard to see how Apple could continue to deliver substantial revenue growth in the years to come. The revenue growth driven by the increase in the average device price came in handy (and helped Apple’s stock price to continue rising for these last few years), but there had to be a natural limit to how much Apple could possibly increase the prices before hitting the ceiling, and now, with nearly $800 in average selling price, it seems the ceiling might finally be close — the most recent news about less than stellar sales of the new, more expensive than ever, iPhones have further confirmed this hypothesis, and led to the extremely sharp decline of the stock price we’ve witnessed over the last few months.

To that point, this is why Apple’s decision to stop reporting the number of devices sold is viewed as troubling by the investors. Even taking Apple’s argument that the number of devices no longer provides a good estimate of the company’s performance at its face value, there would be no reason for it to get rid of this metric now, unless the company doesn’t expect any further substantial and sustained increases in either the number of devices sold, or the average selling price (and thus would then prefer to altogether stop reporting numbers that are set to lack growth)

Finding new growth points

In many ways, the problems Facebook and Apple are currently experiencing are of the same nature. Both companies have sustained impressive growth rates for years, but now, nearing the saturation point, are facing limits to this growth. Both have done a great job monetizing their existing user base, but have no obvious way to continue growing these revenues indefinitely (the situation is a bit more nuanced for Facebook, where this argument mostly applies to its user base in the incumbent markets; more on that later). Finally, both are heavily dependent on a single product generating the majority of their revenues and profits.

And yet, despite all those similarities, what I personally find interesting here is that the future opportunities that Facebook and Apple are facing are actually vastly different. This is also the reason why I’ve previously mentioned that I wanted to compare and contrast these companies — in my opinion, the markets were right to significantly discount Apple’s stock over the last few months (moreover, the previous expansion of P/E multiple in the last few years had been largely unwarranted); on the contrary, Facebook, in my mind, remains to be one of the most undervalued big tech companies right now.

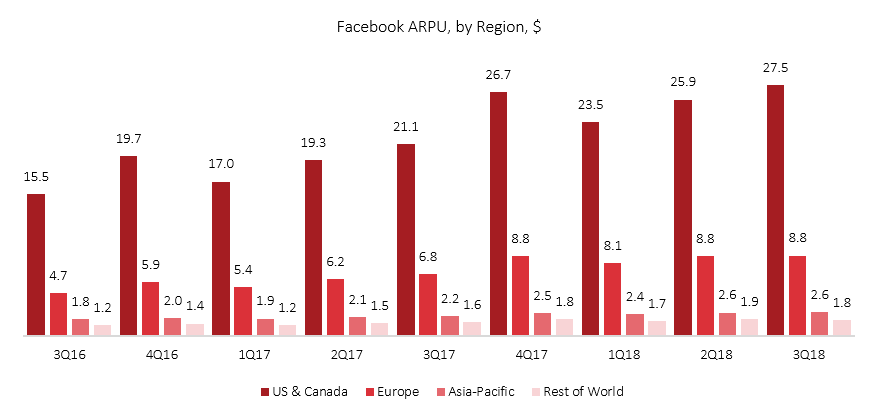

Let’s dig a bit more into that, starting with Facebook. The company effectively holds a monopoly in the social media space: it owns two of the most popular social networks and the most popular global messenger app. While it might be facing limited growth opportunities in North America, it continues to grow its user base in other markets — one might argue that currently, Facebook isn’t doing a great job monetizing its user base outside of North America and Europe, but that could also be viewed as an opportunity, given that Facebook isn’t facing competitive pressure and isn’t losing its users because of its monopoly position in most markets — despite all the recent outrage against Facebook, most users simply have nowhere to go.

Now compare this to Apple. The company is heavily dependent on the sales of a single hardware product (iPhone) that is facing both the ever-increasing competition from Android phones, and also the longer upgrade cycles, simply because the smartphone category is now mature, and the users don’t feel any significant pressure to upgrade frequently. The lock-in effect of Apple ecosystem that helped the company to cross-sell its products is mostly gone — today, nobody has to use iTunes to update iOS devices or to download content on the devices (which arguably acted as a central hub, effectively locking you in the iOS ecosystem, not to mention helping to boost the sales of laptops and desktops running MacOS, considering how terrible iTunes experience on Windows was at one point); besides that, most applications are now cross-platform and sync to the cloud, making switching devices, even the ones running different operating systems, much easier.

True, iPhone as a product still has an army of loyal followers (with me being one of them, actually) and remains one of the best smartphones available in the market. It also continues to benefit from a substantial lock-in effect created by the easy migration to the newest device, and the app ecosystem (on the surface, this statement might seem contradictory to what I wrote in the previous paragraph, but it’s not: what’s gone — and what I was talking about in the previous paragraph — is the opportunity to sell more iPads or MacBooks to people who use iPhones simply because of this fact). So I personally wouldn’t expect iPhone sales to decline going forward, but there is also no substantial opportunity to sell more of them, and, judging by the events of this fall, the opportunity to continue to grow the average price is most likely gone too.

This leaves Apple in a precarious state, as it really needs to find new growth opportunities. Let’s now take a quick look into what those might be.

Services. The revenue from Services in Q4 FY18 reached $10 billion, or 16% of total revenues, — this includes revenue from App Store, AppleCare, Apple Pay, and Apple Music. Apple is forecasting that the revenue drawn from the Services would increase to $14 billion per quarter by FY20, and Morgan Stanley predicts that the revenue growth for the Services would constitute more than 50% of the total revenue growth for Apple going forward, with the idea that the potential for Apple to improve monetization of their existing users, as well as to add additional revenue streams, is very significant.

To be honest, I find this outlook to be all too rosy. It’s true that Apple has already built a truly humongous business in Services (especially with App Store and iTunes/Apple Music), and has the potential to grow it further over time. However, there are several factors that could make scaling Services business at a fast pace challenging, to say the least.

First of all, the idea that Apple’s currently under-monetizing its user base is, in my mind, a fallacy. Unlike Facebook, that doesn’t sell anything to its users, but rather essentially sells their eyeballs to the advertisers (and thus can indeed improve revenue per user, as long as there is sufficient demand from the advertisers, and the space on their website/mobile app to add additional advertisements without ruining user experience), for Apple to improve its user monetization, it needs to sell additional services directly to its users. The problem is, in most cases Apple users aren’t restricted to purchasing their content from Apple, and chances are, if they are interested in certain services, they are already spending their money elsewhere — which means that in order for Apple to grow its Services revenue (esp. without the corresponding increase in hardware sales, and thus the overall user base), it has to convince those users to abandon whatever service providers they are currently using (such as Spotify/Netflix/Amazon), and switch to Apple offerings instead. To an extent, this is a zero-sum game, and it’s not easy to win it, as was demonstrated, for example, by the fact that Spotify user base continues to be substantially larger than Apple’s, despite a huge number of iOS devices that come with pre-installed Apple Music, and years of efforts spent to promote Apple Music on Apple’s part.

The second issue is that Apple simply wasn’t built with the idea of selling Services in mind. Its highly secretive, centralized and hierarchical environment is very well-suited for the purpose of building the best hardware devices, where Apple controls all the aspects of user experience, both on the hardware and software side. However, building a successful Services business is a different story altogether. So far, Apple has proved that it can do a good job curating a catalog of content (meaning App Store and iTunes), and collecting a percentage of revenues from any sales, but, for example, creating a video streaming service would mean competing against extremely data-driven and highly flexible competitors like Netflix and Amazon, which might prove to be very challenging for Apple, not to mention that Apple’s desire to decide what types of content are allowed to be present on its platforms can prove to be really harmful here, as its competitors aren’t held by any such considerations, and there is no evidence that users would appreciate those.

Finally, while the marketplace model of App Store and iTunes remains highly profitable for Apple, that wouldn’t necessarily be the case for the new businesses such as streaming services — Spotify and Netflix can be viewed as two representative examples, with the first company yet to break-even, and the second turning in minuscule profits, while also being saddled with significant debt ($8 billion+ as of September, and counting). What’s even more important, some of the key players in the market (see Amazon) don’t actually need to make their streaming services profitable, — instead, they might offer such services to improve customer retention, and deepen their relationship with the users. The same strategy, in principle, could work for Apple as well, as long as the sales of hardware continued to rise, but it becomes a problem if Services business is now regarded as a growth opportunity for a company whose investors are accustomed to high margins.

iPad. In itself, iPad sales (or the overall tablet market) are unlikely to grow much — while iPad’s initial success had gotten a lot of people to expect tablets to eventually overshadow the traditional PC industry in a similar fashion to what happened with the smartphones, that never came to pass, and over the last few years tablet sales have been largely stagnant or even declining. Part of this is simply the result of the lifecycle of tablets turned out to be much longer than previously thought. Another reason is that the truly valuable use cases for tablets have simply never materialized — the basic entertainment functionality doesn’t require purchasing the newest and most powerful hardware (not to mention that the never-ending increases in smartphone screen sizes turned the category into a formidable competitor to tablets), and the limitations of mobile operating systems restricted the opportunities to abandon laptops in favor of tablets (the fact that the two-in-one devices from Microsoft and its partners offering a combination of full-scale desktop OS experience and tablet inputs continued to get better didn’t help either).

However, I believe that the recent developments in the tablet space have created an interesting and unexpected opportunity that, if executed in the right fashion, might open a valuable new market for Apple.

Gaming. The third generation of iPad Pro that was released earlier this year was equipped with A12X chips — a proprietary 64-bit system on a chip developed by Apple and currently used to power both iPhones and iPads. Apple’s CPUs had been getting better and better throughout the last few years, but the truly outstanding performance of the latest chips was nonetheless a surprise — according to some tests, iPad Pro now boasts a performance comparable to that of the latest generation of 13-inch MacBook Pro which is powered by the most recent Intel processors belonging to the Coffee Lake series. In my mind, this achievement could now open a path to some pretty exciting new opportunities for Apple.

The gaming industry in 2017 was approaching $110 billion in annual revenues, with Mobile accounting for $46 billion (tablets brought in a bit less than 25% of that), and consoles representing the second largest segment, estimated at $33.5 billion. Apple already draws very decent revenues from gaming on smartphone and tablets, but the incredible performance of its newest chips, coupled with the success that Nintendo Switch has seen over the last 2 years (it sold 20 million devices in 15 months, which, according to some estimates, is on par or better than the sales numbers for PS4 at the same point of its lifecycle), indicates that there is a very clear demand for a more serious portable gaming devices, and Apple might just have the tech necessary to build such product.

To be fair, I am not saying that this would be easy to do, or that Apple is necessarily the right company to execute on such an opportunity. Building a console business would likely require Apple to learn how to collaborate with the largest game studios much more closely than it currently does, and possibly would also mean that it would need to build its own production and publishing business, similar to what Microsoft currently does with Microsoft Studios; it might also face challenges creating a device that provides gamers with an experience comparable or superior to the one currently offered by the Switch, given Apple’s relative lack of expertise in the field (although it’s worth noting that Apple already made a couple of attempts to expand into the space, so it won’t be completely clueless).

And yet, I would argue that Apple stands a much better chance of expanding its presence in gaming, than it does, say, building a successful streaming service, as its success in gaming would rely on the very same capabilities that made Apple so successful in the first place, namely, manufacturing a hardware product that offers users a superior experience through a tight integration of hardware and software, whereas creating a streaming service (and the same is true for some of the other businesses that can be classified as Services) often requires capabilities that Apple currently doesn’t possess.

The final question here would be, if Apple enters the console gaming space and manages to build a successful presence there, would it help the company to alleviate concerns about future growth? That remains to be seen: first of all, right now Apple hasn’t publicly announced any intention to do so, therefore, everything described above remains speculation on my part. Second, even if it manages to eventually replicate the success of Nintendo Switch, it would still need to build a huge business in the area for it to start making a difference in the broader context of the company’s financial performance.

To put Nintendo Switch numbers into context, 20 million devices sold at $300 retail price means bringing in $6 billion in revenues, which is a great deal of money for Nintendo, but not so much for Apple — therefore, it would likely need to do even better for this opportunity to be really worth it. However, the Gaming market is growing at a healthy pace, and the revenues from devices are not the only possible revenue stream here (production and publishing of gaming is another one; so is streaming), so in the long term, it might indeed turn out to be Apple’s best bet for growth.

MacOS. I believe the chance that macOS would present any substantial growth opportunities for Apple going forward is very low; rather, it’s actually much more probable that the revenue share of the desktops and laptops in the overall mix would continue to decline. The introduction of iMac Pro in 2017 represented an interesting development, but it remains a niche product, with limited appeal to the wider audience, and the rest of the updates over the last few years were thoroughly unexciting. There is a small chance that the rumored upcoming switch to ARM processors would help Apple to create a more differentiated offering in the space, but even then, the chances of a substantial growth coming from this segment remain slim.

Apple Watch and AirPods. Apple Watch is arguably the most successful wearable device today, but at this point, the category is fairly mature, and while in Q4 FY18 Apple reported a 50% growth in revenues for the category year over year, going forward the growth would be slower.

AirPods, however, represent a different case — according to some estimates, Apple will sell 26 to 28 million units in 2018, vs. 14 to 16 million in 2017, which represents a growth rate of 62% to 100%, and could continue to aggressively grow the category, potentially reaching 100 to 110 million units in annual sales by 2021. If that turns out to be the case, Apple could draw an annual revenue of up to $18 billion from this category.

On the surface, that’s a huge number, but in Apple’s case, the same argument I made about Gaming above applies here: even $18 billion in annual revenues would constitute only about 6.5% of Apple’s total revenue for FY 2018, and 6.1% of $294 billion in revenues forecasted by Morgan Stanley for 2021, which means that AirPods, however successful, might not become a category that is large enough to make a real difference going forward. Still, right now, AirPods might actually be Apple’s best bet for short-term growth.

And this brings us to the final conclusion:

Facing the future

In my opinion, it would be a mistake to either underestimate or overestimate the scale and seriousness of the challenges Apple’s facing today. On the one hand, Apple today remains one of the most successful tech companies in the world, and it is highly likely that the business it has built will continue to bring in huge profits for years to come, — to that point, the predictions of Apple’s inevitable demise are very unlikely to materialize. On the other hand, tech companies today are to a very significant extent judged by their ability to continue to grow (indefinitely, if possible), and that’s where Apple is likely to face serious, if not altogether insurmountable, challenges.

Yes, there are some promising opportunities that the company can execute upon with its existing products and capabilities — Gaming and AirPods being the two that in mind represent the most attractive targets. But even if both of those would pan out, the main issue Apple is facing today stems from its sheer size — it is really hard to find opportunities that are large enough to make a difference for a company with an annual revenue of over $260 billion (with AirPods being a great illustration of the issue - even if the wildest forecasts would prove to be true, it would remain a small percentage of the company’s overall revenue).

What Apple really needs, if it has any hopes of continuing to grow at the pace it has enjoyed over the last 15 years or so, is to find another opportunity of the iPhone-like size that also aligns well with the company’s know-how and the organizational capabilities. The problem is, such opportunities are so extremely rare that there is simply no guarantee that one would emerge over the next decade, not to mention that even if it does, there is a good chance that Apple wouldn’t be the best organization to act upon it. And this is the key thing that distinguishes Apple from Facebook — the latter doesn’t really need to go look for new opportunities (not that they shouldn’t search for those, of course, but there is no immediate pressure to do so), but rather has the luxury to focus on their existing products, while for Apple it is an economic imperative, if the company wants to continue to grow.

Disclosure: This article expresses my own opinions, and my opinions only. I am not receiving any compensation for it. I have no business relationship with either Facebook or Apple. I hold no position in Apple stock, and a long position in Facebook stock, and have no plans to adjust those positions or initiate new ones within the next 72 hours.