It’s been a while since I’ve published anything here — hopefully, it’ll now change. I’m looking forward to get back to writing on a regular basis, aiming for a post per week or so.

This is the first part of a 2-post series. The second article can be found here.

An IPO priced at $104 billion, followed by the company’s valuation dipping below $50 billion within 3 months, and then recouping all losses in a year, and never stopping ever since, with its valuation peaking at over $600 billion this year. Recognize the company? I bet you do — this is, of course, Facebook.

Where does one go from 2 billion users?

As with any platform relying on the advertising revenue, there are 4 key metrics Facebook’s performance relies upon: number of active users on the platform, time they spend there daily/monthly, advertising space utilization (with 2 aspects associated with it — e.g. whether it’s possible to add more advertising blocks per screen, or sell a higher percentage of the existing ones), and, finally, price per ad. It’s worth noting that the last metric — price per ad — often isn’t really an independent one, in a sense that unless the utilization is at capacity, and is coupled with excess demand, thus creating scarcity for the advertising space, it’s unlikely that price per ad would increase on its own (and even then, the price per ad is still subject to the competition from other platforms).

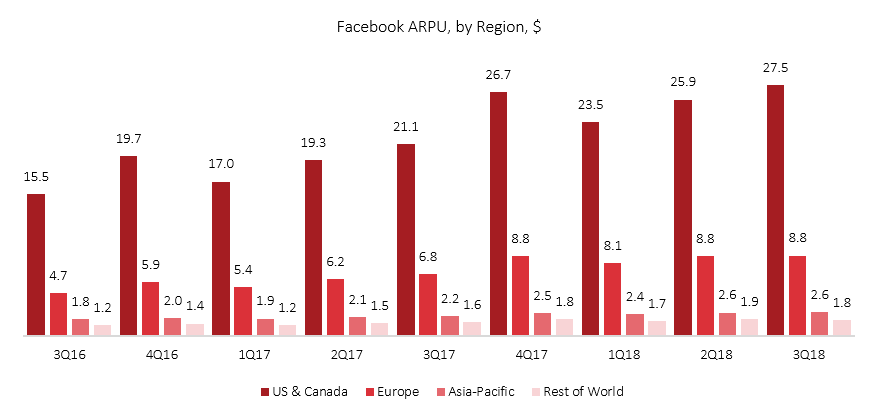

Source: Facebook Q3 2018 Earnings Presentation

Now, when Facebook went public in May 2012, it had around 900 million monthly active users, and a bit over $1 billion in quarterly revenue. Today, the number of users has increased to 2.27 billion, while the revenue has grown to $13.7 billion. Granted, not all in 2018 not all of Facebook’s revenue is coming from Facebook.com — while the company doesn’t break out Instagram’s revenue, it’s estimated to have reached about $2 billion per quarter this year, and is posed to continue to grow. Still, it’s obvious that since 2012, Facebook has significantly ramped up its efforts to monetize its user base, to a point where it appears that it can no longer increase the number of ads in the News Feed. That, coupled with the slowing user growth (which came almost to a halt in its most lucrative markets — Europe, US & Canada — in the recent quarters), makes it challenging for Facebook to continue growing revenue at the same pace in the future.

Source: Facebook Q3 2018 Earnings Presentation

Concerns over the slowing revenue growth, and revised guidance for the upcoming quarters were the main reason for an extremely sharp decline of 20%+ in Facebook’s stock price in July, after it announced Q2 results. Granted, the Cambridge Analytica scandal and overall concerns over privacy probably didn’t help either; however, it’s worth noting that by the second half of July Facebook was back to trading at an all times high, so it seems unlikely that either Cambridge Analytica incident, or the privacy concerns had much to do with the drop in stock price that followed Q2 earnings announcement.

Reported on October 30, Q3 earnings did little to dissuade investors’ concerns over the company’s ability to continue to grow at a fast pace: while Facebook exceeded the expectations for earnings, it missed forecasts on revenue and DAUs/MAUs, which arguably are more indicative of the growth potential. It’s therefore curious that despite of that, the market didn’t register any further decline in the stock price (although there were a couple of wild swings before the price settled at more or less the same levels as before the earnings’ announcement). That being said, given that the current price of ~$145 per share is 18% lower than the $176 per share after the disastrous announcement of Q2 earnings, and 33% lower than 2018 peak price, one could argue that the not so stellar results of Q3 were simply already baked into the stock’s price.

Now, it’s obvious that Facebook in 2018 is quite different from what the company it was back in 2013, when its stock started its mind-blowing ascent (close to 10 times returns in 5 years, from July 2013 to July 2018). Many of the concerns surrounding Facebook’s potential to continue to grow are justified, and require addressing. And yet, at 22x P/E, Facebook appears to be much cheaper than most of the other big tech companies: for instance, Google is currently traded at 42x P/E, Netflix at 108x, Microsoft at 45x, and Amazon at 96x (to be fair, P/E isn’t always a good benchmark to use to compare valuations, but in this case, the discrepancy between the Facebook’s valuation and that of others is too substantial to be ignored, even if the metric itself is flawed).

Some might notice that one company is conspicuously absent from the list above. That company is, of course, Apple, which represents another potentially interesting case, as it’s currently trading slightly above 17x P/E.

It might indeed be worth spending some time to dig into Apple here. In many ways, the problems Facebook and Apple are currently experiencing are of the same nature. Both companies have sustained impressive growth rates for years, but now, nearing the saturation point, are facing limits to this growth. Both have done a great job monetizing their existing user base, but have no obvious way to continue to grow those revenues indefinitely. Finally, both are heavily dependent on a single product generating the majority of their revenues and profits.

And yet, despite all those similarities, what I personally find particularly interesting here is that the future opportunities that Facebook and Apple are likely to face are actually vastly different.

Side note: Apple was originally supposed to be a part of this article, with me intending to cover both Facebook and Apple in one post. However, since it was getting way too long, I’ve decided to split this article in two, therefore Apple would be covered in the next piece.

Growing beyond original limitations

I think it would be fair to state that Facebook.com is unlikely to grow its MAUs much further, and the opportunities to monetize the geographies where it is still acquiring new users are likely to lag behind those of North America and Europe. The lagging monetization of the new content formats, namely Stories, represents another growing problem for the company.

That being said, however, it seems unwise to underestimate just how well protected Facebook’s market position currently is.

At the time of its public offering in 2012, Facebook’s monopoly on the market wasn’t yet solidified. Since then, however, it managed to acquire and then very successfully scale Instagram, which arguably would have represented its strongest competitor otherwise; it also removed the threat of WhatsApp by acquiring it, and managed to copy and then improve on some of the key features of Snap that are now available both on Facebook and on Instagram, thus crippling its ability to grow or retain its user base. All that, coupled with the decline of some of the stronger regional social networks (e.g. VK.com and Orkut), left users with no alternative but to continue to use Facebook’s properties (which includes Instagram and WhatsApp). You do, of course, still have Twitter and LinkedIn, but the nature of those networks is substantially different from Facebook, to point where it could be fair to argue that the common scenarios all three of those could possibly compete for are exceedingly rare.

Another trend that, while doing Facebook some (limited) harm short-term, might be actually helping to further entrench the company as a market leader is the current push towards privacy. Today, with the developers no longer enjoying the freedom of access to the entire Facebook’s social graph as they did in the earlier years, it becomes even more challenging for any aspiring competitor to scale its services, as it now has to compete against the incumbent whose services are already being used by everyone (and that is thus enjoying tremendous network effects), and at the same time can no longer piggyback on Facebook’s social graph for its benefit.

The same goes for regulations like GDPR — instead of, or rather, in addition to, putting oversight over what tech giants can and cannot do, it also makes it much more challenging for the data to flow freely, which (surprise!) helps incumbents the most, and actively harms smaller startups that are often dependent on 3rd-party user data being shared with them — which is exactly why, as I wrote previously, I believe GDPR stands to do more harm than good, and other countries, including the U.S., would do well to be wary of implementing similar regulatory frameworks (that’s not to say that privacy isn’t important — but it’s crucial to clearly understand the trade-offs you’re making).

In that sense, while Facebook might be currently struggling to monetize some of its geographies and/or content formats, the one thing (and an extremely unusual one for a tech company to have too) it has is time, as it has by now all but eliminated competition, and its network effects are simply too strong for any new players to successfully compete against it. That, of course, doesn’t mean that no company could ever unseat Facebook from its throne as the king of social, but it could be a long time before anyone figures a way to do that, which leaves Facebook an opportunity to continue to extract rents from its user base, while also figuring better ways to do so.

Finally, Ben Thompson made an interesting point in his August post about Facebook: it’s possible that the new content formats, and Stories in particular, might eventually allow Facebook to finally tap into the brand advertising market, unlocking a huge market that the company hasn’t been able to substantially penetrate yet. If that turns out the case, a short-term hit associated with the limited opportunities to monetize Stories Facebook has to take now would be more than worth it in the longer term — and indeed, intentionally pushing the customers towards Stories, even it means sacrificing some of the revenue from the News Feed, might prove to be exactly the right strategy.

Still a great opportunity

Source: Macrotrends.net

To that end, I believe that Facebook today is considerably undervalued, compared to its big tech peers. While the company has a number of issues to work through, some of which weren’t apparent earlier (which might justify some of the correction in stock price we’ve witnessed), none of the fundamentals have really changed in 2018, which makes the extremely aggressive decline in P/E ratio this year (or even more generally, over the last 3 years) hard to justify.

After all, Facebook remains the largest social platform on the planet, and, in many cases, the only viable option, with plenty of opportunities for growth, and, more importantly, the luxury of having the time to figure out how to execute on those (again, the time here is simply a function of the lack of alternatives to Facebook/Instagram from the users’ perspective), which is really a rare thing in the tech space.

Disclosure: This article expresses my own opinions, and my opinions only. I am not receiving any compensation for it. I have no business relationship with either Facebook, or Apple. I hold no position in Apple stock, and a small position in Facebook stock, and have no plans to adjust my position(-s) or initiate new ones within the next 72 hours.